The Role of Hydrogen in the Visegrad Group Approach to Energy Transition

Faculty of Social Sciences, Institute of Politics and Security Sciences, University of Szczecin, 71-017 Szczecin, Poland

Energies 2022, 15(19), 7235; https://doi.org/10.3390/en15197235

Submission received: 9 August 2022

/

Revised: 14 September 2022

/

Accepted: 16 September 2022

/

Published: 1 October 2022

(This article belongs to the Special Issue Transformation of Energy Systems: From the Perspective of Climate and Energy Policies)

Abstract

:Hydrogen is an energy carrier in which hopes are placed for an easier achievement of climate neutrality. Together with electrification, energy efficiency development, and RES, hydrogen is expected to enable the ambitious energy goals of the European Green Deal. Hence, the aim of the article is to query the development of the hydrogen economy in the Visegrad Group countries (V4). The study considers six diagnostic features: sources of hydrogen production, hydrogen legislation, financial mechanisms, objectives included in the hydrogen strategy, environmental impact of H2, and costs of green hydrogen investments. The analysis also allowed to indicate the role that hydrogen will play in the energy transition process of the V4 countries. The analysis shows that the V4 countries have similar approaches to the development of the hydrogen market, but the hydrogen strategies published by each of the Visegrad countries are not the same. Each document sets goals based on the hydrogen production to date and the specifics of the domestic energy and transport sectors, as there are no solutions that are equally effective for all. Poland’s hydrogen strategy definitely stands out the strongest.

1. Introduction

The energy transition is gaining momentum, and climate policy has catalyzed the development and deployment of renewable energy sources (RES). Thanks to appropriate regulations adopted by the European Union (EU), the continent should achieve climate neutrality by 2050, which means that in less than three decades the EU economy is expected to produce as much greenhouse gases as it can absorb [1]. However, the transition to zero-carbon energy sources is taking place at different speeds across EU member states. This is due to the emergence of barriers that hinder them from achieving sustainable development [2]. This is due to the historical ties of the countries, especially those in Central Europe, which have influenced their choice of energy sector development paths. Recently, the V4 countries have been openly expressing their concerns and preferences for maintaining energy security of both their own country and the region as a whole. Actions taken to further support the development of nuclear energy, the implementation of natural gas diversification projects or criticism of the European Green Deal strategy are evidence of the individual approach of these countries to changes promoted by the European Union [3]. In this context, the development of hydrogen economy seems particularly important. Hydrogen may in the near future make it easier to meet the exorbitant climate requirements of the EU.

In 2021, the Visegrad Group countries adopted hydrogen strategies following the entry into force of the EU Hydrogen Strategy, which gave rise to an examination of the current degree and prospects for the development of this technology. This article aims to query the development of the hydrogen economy in each of the V4 member states. In addition, the study will make it possible to determine the role that hydrogen will play in the energy transition process. The following research questions serve to achieve the stated aim:

- 1.

- What are the characteristics of the hydrogen strategies of the V4 group?

- 2.

- How will the development of the hydrogen economy in the Visegrad countries evolve?

- 3.

- What will be the impact of hydrogen sector development on the energy transition process in the V4 countries?

The article consists of six parts. After the introduction, the theoretical background of the development and application of hydrogen technology is presented. Section 3 presents the methods used in writing the article. Section 4 contains an analysis of the hydrogen strategies of each V4 member state. Section 5 discusses the results of the comparative analysis, and the last part of the article is conclusions.

2. Literature Review

Hydrogen is a fuel that has been used for several decades in many sectors of the economy. However, it is only the process of energy transformation which made many countries express renewed interest in hydrogen as an alternative to fossil fuels [4].

Hydrogen is an attractive option that will mitigate climate change risks and help the energy transition due to its chemical and physical properties. Hydrogen is the source of the largest amount of energy per unit mass of any known fuel; its energy per unit mass is three times that of gasoline. However, this element does not exist on Earth in gaseous form [5]. On our planet, it occurs only in complex form, in combination with other elements. In addition, it occurs in the form of water due to the reaction with oxygen, in combination with carbon, in organic compounds, among others in hydrocarbons (oil, coal, methane) and in all plant and animal organisms, which are counted as biomass [6].

As history shows, the first recorded production of hydrogen took place in the 15th century, when the medieval physician Theophrastus Paracelsus, while examining chemical substances for use as medicines, dissolved iron in sulfuric acid, thus producing hydrogen gas. However, hydrogen had to wait until the 18th century for a formal classification and description [7]. Hydrogen was then used as an industrial chemical. The use of hydrogen as an energy carrier is not a 21st century invention. The earliest attempts to use it in automobiles date back to the time of Napoleon Bonaparte. In 1807, Swiss Isaac de Rivaz constructed the first wheeled vehicle powered by a hydrogen engine, which allowed the vehicle to move 6 m [8]. In 1874, Jules Verne, among others, proposed the use of hydrogen as a fuel by describing a hydrogen-powered economy in his book The Mysterious Island. Hydrogen was also used for street lighting or in lamp structures [9].

The use of hydrogen is usually associated with the airship disasters of the 1930s. However, it is worth noting that these were designed for helium, and the use of hydrogen in German airships was an emergency solution. The United States, the helium potentate at the time, did not want to sell it to Germany, so the Germans were forced to use hydrogen, which was easier to obtain and cheaper than helium. After World War II, affordable oil prices halted the development of this technology [10].

Hydrogen, together with renewable energy sources, will be an effective weapon in the fight against global warming and thus contribute to reducing greenhouse gas emissions. An important feature of H2 is having the highest energy content of any conventional weight fuel at 120 MJ/kg (for example—coal is 25 MJ/kg, gasoline 47 MJ/kg). Still, on the other hand, it has the lowest energy content by volume (3 kWh/m3 at 20 °C and 1 bar), which is a limitation for transport, (a tank that can hold e.g., 6.3 kg of hydrogen has a total capacity of 156 L) [11,12,13]. On the other hand, due to the fact that the hydrogen tank has 10 times the greater energy density than the battery, this carrier is prospective for the development of the long-distance vehicle market [14].

Storing hydrogen remains a challenge. Hydrogen has a very low density: 1 kg of hydrogen takes up more than 11 m3 at room temperature and atmospheric pressure, which is a major obstacle to its efficient storage. Therefore, to make conventional high-pressure and/or low-temperature hydrogen gas or liquid storage economically viable, its storage density needs to be increased, and therefore research is constantly carried out [15,16].

Currently, there are several different technological options for large-scale hydrogen storage, which can be divided into three categories:

- Hydrogen can be stored as a gas or a liquid in molecular form (liquid and compressed hydrogen);

- Molecular hydrogen can be adsorbed on or in a material held in place by relatively weak physical van der Waals bonds (hydrogen adsorption);

Currently, it is possible to store hydrogen underground in salt caverns or depleted oil or gas fields, or in deep aquifers. [18]. The use of hydrogen for energy storage will help to stabilize the energy system, especially in the context of surplus renewable energy production, whose reception into the grid is then limited. In such a situation, excess electricity can be used to produce hydrogen, acting as a chemical energy storage [19]. Thirdly, hydrogen is considered to be a highly efficient and low-pollution fuel because hydrogen fuel cells produce electricity during the chemical reaction that occurs when hydrogen comes into contact with oxygen, with water and heat being the only by-products. Therefore, this element can be used in transportation or for heating and power generation, especially in industries where the electrification process is difficult due to various restrictions (heavy transport or maritime transport) [20]. However, it is worth mentioning that hydrogen production processes are not entirely environmentally friendly. Due to the production method, the following terms for hydrogen are used:

- -

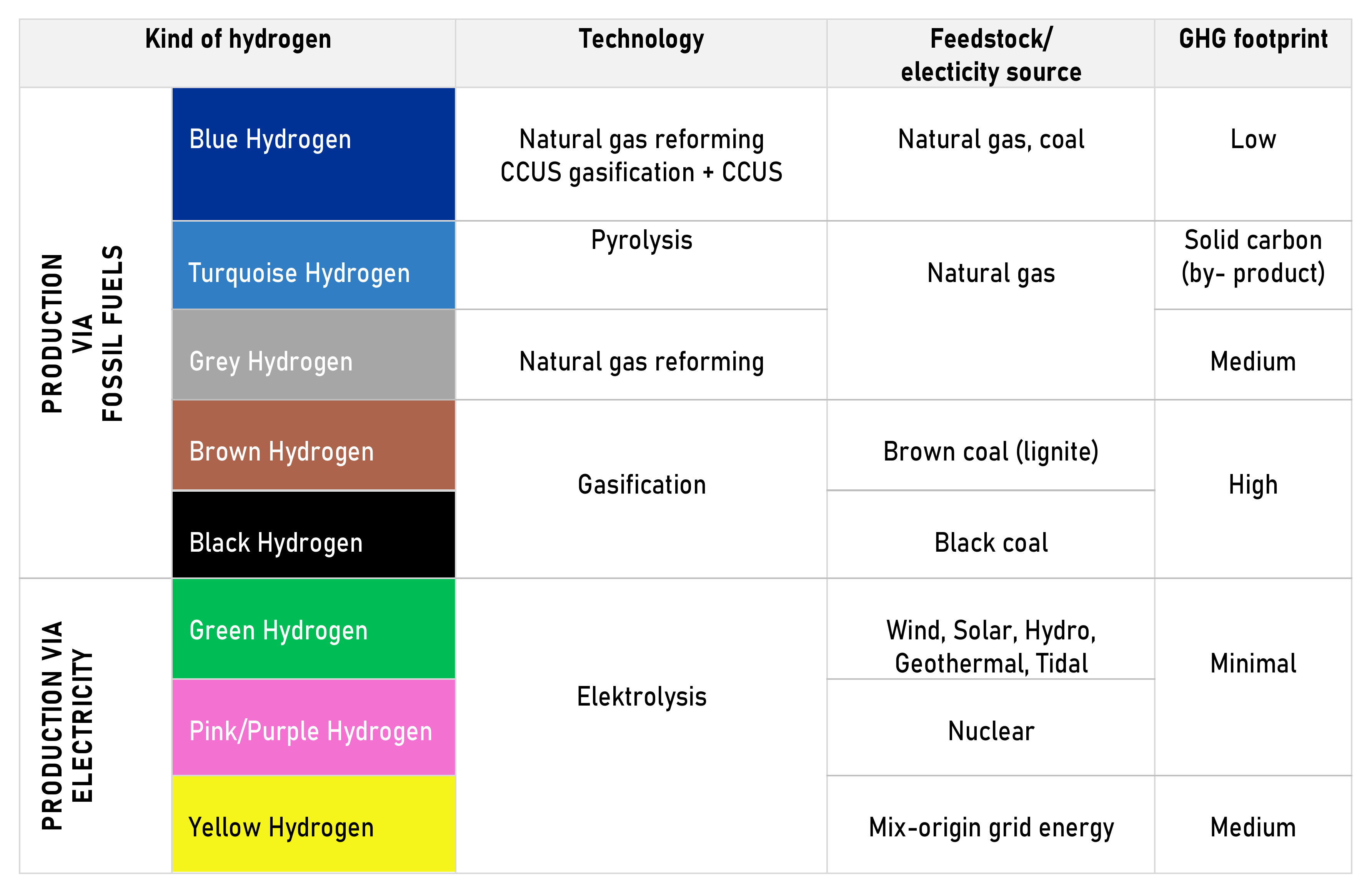

- Grey hydrogen: Obtained from fossil fuels using the energy from such fuels, and whose production is associated with high CO2 emissions,

- -

- Blue hydrogen: Obtained in a similar way to grey hydrogen, except that the process is combined with CO2 capture and storage (CCS) technology,

- -

In the rainbow of colors of hydrogen, there are also: black and brown hydrogen; the first one comes from the conversion of hard coal and the second one from brown coal. Apart from that, there are pink hydrogen resulting from the electrolysis of water powered by nuclear energy, yellow hydrogen produced from the electrolysis of water using solar energy, and turquoise, which is a product of methane pyrolysis, which leads to the production of pure hydrogen and solid-phase carbon (no emissions or need to capture CO2) [23].

The classification of hydrogen based on these colors describes its environmental friendliness. Thus, green hydrogen is considered clean, and its production does not harm the environment, grey hydrogen production can be a significant burden on the environment, while the impact of blue hydrogen production is between green and grey [24] (Figure 1).

Hydrogen is an energy carrier and can be produced from a variety of energy sources. In 2020, the global production of hydrogen was 120 million tons of hydrogen of which 80 million tons is pure hydrogen and the rest is a mixture of hydrogen with other gases, used in the production of steel or methane [25].

Fossil fuels account for the largest share of hydrogen production (over 80% of production), mainly natural gas, and to a lesser extent oil and coal [26]. Like natural gas, hydrogen can be compressed and transported over long distances. It is worth mentioning that it can be mixed in the right proportions with natural gas, which feeds gas networks, or it can be converted into methane, or ammonia used in thermal power generation. Hydrogen has been used in various industries for many years. In refineries, it is used for hydrocracking and desulfurization of diesel fuels. In the chemical industry it is used to produce ammonia and fertilizers for agriculture. In addition it is also used in metal and fabrication, food processing, and electronics [27]. In 2020, the hydrogen industry was valued at nearly $121 billion, and its value is steadily increasing as interest in the element increases [28].

The greatest hopes are pinned on the so-called green hydrogen, which appears to be a flexible carrier mitigating the negative effects of the energy transition. The process of obtaining green hydrogen uses the phenomenon of electrolysis, during which water is split into hydrogen and oxygen. Then, hydrogen becomes a renewable energy carrier [30].

With this method, electricity consumption can be adjusted to wind and solar power generation, and hydrogen becomes a source of storage for electricity produced from RES [25]. Electrolysis can occur at both low and high temperatures [31].

Carbohydrate-rich biomass could be another important source of green hydrogen. There are two main categories of hydrogen production from biomass: thermochemical and biological methods. [32]. Lignocellulosic biomass (e.g., wood, straw, grasses) is currently the most available biomass resource for the production of biohydrogen, although it has its drawbacks (production of potential fermentation inhibitors, applied pre-treatment process). On the other hand, microalgae and macroalgae represent the third-generation raw material for hydrogen production, and wastewater treatment in the dark fermentation process and aqueous-phase reforming of biomass are interesting alternatives under research [33].

Hydrogen derived from green energy can contribute to a new renewable energy market. By using hydrogen, RES power generators have the opportunity to reduce the risk of energy price changeability when some or all of the production is sold to electrolyser operators under long-term contracts [27]. In the low-carbon future toward which the European Union is moving, hydrogen offers new roads for valorizing renewables. Renewable hydrogen has the technical potential to direct large amounts of electricity to sectors where decarbonization is difficult [34]. Thus, the versatility of the use of hydrogen explains the increased interest in this energy carrier among many countries, which translates into a desire to use it in the near future as an important part of the energy transition.

3. Methodology

The methodology used in this thesis is in line with the stated research objective. The methodological approach in this study is mainly based on literature review, description of hydrogen strategies of V4 countries, their quantification and comparison. The main step of the methodology is the comparison of hydrogen strategies taking into account six diagnostic features: sources of hydrogen production, hydrogen legislation, financial mechanisms, objectives included in the hydrogen strategy, environmental impact of hydrogen and costs of zero-carbon hydrogen investments. The timeframe of the study was set to 2021–2030, as the timeframe in the hydrogen strategies discussed is not uniform. Moreover, all four documents best detail hydrogen market development activities just for the next decade.

The study used the integrated literature review method, which allowed for the grouping of literature sources based on the conceptual criteria adopted. The application of the comparative method allowed comparing data related to activities aimed at the development of the hydrogen economy in the V4 countries. The applied research methods allowed answering the set research questions. The comparison of forecasts of the sources of hydrogen production, as well as its volume, strategic goals, support mechanisms, and legal environment, allows drawing conclusions on the research question concerning the development of the hydrogen market in the region; it also helps to answer the question regarding the role hydrogen will play in the process of energy transition in the V4 countries. The study also employs research techniques, such as analysis, description, verification, and forecasting. The conducted research was based on strategic documents regarding the development of the hydrogen market, i.e., on the hydrogen strategies of each of the V4 countries, and on the hydrogen brochure issued for each country separately by the EU. The ScienceDirect database of scientific articles was mainly used to obtain information on hydrogen.

4. Hydrogen Strategies of the Visegrad Countries

Achieving climate neutrality by the middle of this century has become a priority for EU leaders. To this end, on 8 July 2020, the European Commission (EC) adopted a hydrogen strategy, as hydrogen is to be a key energy carrier from the perspective of EU efforts to create a new green deal in Europe. The main goal of the strategy is to stimulate the development of renewable, green hydrogen so that by 2050 it will be a fully zero-emission, widely available energy source in the EU. At the same time, the EC recognizes that in the short to medium term, to ensure the development of the hydrogen market, it is necessary to allow the use of other low-carbon forms of hydrogen in Europe (extracted from fossil fuels in combination with carbon capture and storage technology—CCS—or by electrolysis using non-renewable sources). However, low-carbon hydrogen is to be a transitional solution, after 2050 only zero-carbon hydrogen will be used [35]. The above strategy is the most ambitious document for green hydrogen development in the world, predicting 40 GW of green hydrogen production by 2030 in the EU [36].

In 2020, almost 7 million tonnes of H2 were produced in the European Union, (2 million tonnes in Germany, 1.5 million in the Netherlands, 1.3 million in Poland, and 0.5 million in Spain). These four countries account for 50% of total EU, EFTA, and UK hydrogen production [37]. Within a few years, the above ranking may change as some countries, such as France, Italy, and Sweden, have included high targets for green hydrogen production capacity in their hydrogen strategies [38].

4.1. Poland

Poland is one of the largest producers of hydrogen in the world, ranking 5th in the world and 3rd in the European Union [37], with an annual production of about 1.3 million tons. Hydrogen production takes place mainly in large industrial plants in the process of steam reforming of hydrocarbons, where hydrogen is used in industrial processes [39]. Currently, the largest producer of hydrogen in Poland is a chemical consortium, Grupa Azoty SA, which produces about 420,000 tons of hydrogen per year and its share in the hydrogen production market reaches 32.3%. The following oil companies are also significant producers of hydrogen: Polski Koncern Naftowy Orlen SA and Grupa Lotos SA with 11% and with 4.5% share of the hydrogen market, respectively, and Coking plants (Koksownia Przyjaźń, companies from Jastrzębska Spółka Węglowa SA Capital Group and Koksownia Zdzieszowice) with 11.5% share [40]. However, all of this production is grey hydrogen, produced from fossil fuels and CO2 [41].

The development of the hydrogen market in Poland is of particular importance, and hydrogen seems to be a remedy for the current energy and climate problems. Hence, hydrogen is supposed to help Poland, at least partially, jump the intermediate stage of large generation of energy and heat from natural gas, which Poland has not yet entered, especially since gas has become very expensive. The Polish Hydrogen Strategy (PSW) indicates the role of hydrogen, which is to serve as an energy store and enable balancing of the power grid, as well as enable reduction of emissions in sectors where electrification is not economically justified. In addition, the PSW describes opportunities and sets tasks in six areas:

- Deployment of hydrogen technologies in power and heating (by 2025, Power-to-hydrogen (P2H) installations with a total capacity of 1 MW will be put into operation, as well as the co-firing of hydrogen in gas turbines and the development of energy storage based on hydrogen technologies will begin);

- Use of hydrogen as an alternative fuel in transport (by 2025, Poland will have at least 100 hydrogen buses in its fleet, and by 2030 their number may increase tenfold; it is also assumed that 32 hydrogen filling stations will be built, and in 2025 the first hydrogen trains will appear on Polish rails)

- Support for decarbonization of industry (by 2025, implementation of pilot technological projects for application of low-emission hydrogen in the petrochemical, chemical and fertilizer sector and other energy-intensive industries. At least five hydrogen valleys will be established in Poland by 2030, and the investments made in them will be included in a common European infrastructure);

- Production of hydrogen in new installations (by 2025, production of synthetic gases in the process of methanizing hydrogen and use of low-emission hydrogen in production of ammonia will be launched. Low-carbon hydrogen production facilities with a total capacity of at least 50 MW will also be built. Their total capacity in 2030 is expected to reach 2 GW);

- Efficient and safe transmission, distribution, and storage of hydrogen (a feasibility study of a hydrogen north-south pipeline is to be prepared by 2025. The existing gas infrastructure is also to be examined in terms of possibilities for hydrogen injection and transmission of hydrogen-gas mixtures. By 2030, research is also to be conducted on the development of large-scale salt caverns for hydrogen storage, as well as the introduction of synthetic methane produced in P2G systems into gas networks);

- Creation of a stable regulatory environment (development in 2022–2023 of a legislative hydrogen regulations package specifying the details of market operations, implementing EU law in this area and implementing a system of incentives for low-emission hydrogen production) [21].

4.2. Czech Republic

Hydrogen technology development work in the Czech Republic began five decades ago, in 1960. In the 1970s and 1980s, this activity was stopped. However, proper foundations along with technical and technological facilities allowed the restoration of hydrogen activities in the 1990s. In 2007, the Czech Hydrogen Technology Platform HTYEP was established, and the first demonstration projects were implemented. It is worth mentioning that the above hydrogen technology development was not coordinated or guided by a national strategy, but by individual actions or bilateral cooperation [42]. Only since 2015 has there been a significant increase in interest in hydrogen, the ultimate expression of which is the Czech Hydrogen Strategy (CSW) adopted by the Government in 2021. There are a number of regional initiatives developing hydrogen technology in the Czech Republic. One example is the Ustecky region, which, together with Orlen Unipetrol, has begun working with a group of 17 public and private entities in a collaborative effort to support the development and use of hydrogen in local industry. Furthermore, the Ustecky region is the first region in the Czech Republic to join the S3 European Hydrogen Valleys partnership [43,44].

The Czech Republic produces over 900 million m3 of hydrogen annually, which is mainly produced from fossil fuels and consumed for domestic needs, the remaining domestic demand is supplied by imports, mainly from Poland, Germany and Slovakia [45]. The Czech Hydrogen Strategy introduces four areas around which the hydrogen market will be developed.

- Production of low-carbon hydrogen

- Consumption of low-emission hydrogen

- Transportation and storage of hydrogen

- Development of new hydrogen technologies

In addition, activities within the above areas will be carried out in three time periods (so-called phases). Phase 1 covers the period from 2021 to 2025, and its main objective is the use of hydrogen in transportation. As early as in 2015, in the Czech Republic, The National Action Plan for Clean Mobility was prepared, which sets goals related to the development of clean technologies and their use in transport [43].

As part of this program, the government pledged to support companies with funding that would be used, among other things, to build the first charging stations for hydrogen vehicles (CZK 150 million was initially allocated for this purpose, and in 2019—additional CZK 1.2 billion). The government’s aspiration is to build 6–8 stations by 2023, and 15 by 2025 [46]. In addition, testing of existing gas infrastructure will begin, as part of its adaptation to hydrogen transmission. The use of renewable energy sources will play an important role in this phase. Phase 2 is for the next five years, during which Czech policymakers expect that verification of industrial use of hydrogen will begin. Its scale will depend on the success of the development of systems for the pyrolytic decomposition of organic waste and natural gas, and the construction of large local solar or wind power plants combined with electrolyzers and facilities for compressing or liquefying the hydrogen produced. In addition, planning will also begin on how to transport and distribute hydrogen, including opening up the possibility of contracting for the construction of new hydrogen pipelines or the conversion of existing gas pipelines into hydrogen pipelines for both domestic transport and transit through the Czech Republic. Based on technological advances, it will also be possible to consider the construction of new nuclear sources, including small modular reactors that would use most of their capacity to produce low-carbon hydrogen. Due to the energy needs of industry and the lack of low-carbon electricity sources, the Czech Republic is expected to be a net importer of hydrogen, as is currently the case for natural gas and oil. In parallel, testing of hydrogen supply for domestic consumption should begin in this phase. Domestic production of hydrogen vehicles is expected to begin during this phase. The final phase covers a 20-year time horizon (2031–2050). During this phase, pipeline/network hydrogen transportation will operate without state subsidies. True mass industrial deployment of hydrogen technologies will only be possible after the construction of a hydrogen pipeline network that will supply the Czech Republic with low-cost low-carbon hydrogen from abroad and allow its distribution to necessary locations. At the same time, local hydrogen distribution networks will be established to supply households with hydrogen instead of gas [47].

4.3. Slovakia

Slovakia, like Poland and the Czech Republic, considers it necessary to implement hydrogen technology, which will increase the competitiveness of the Slovak economy and, at the same time, make a significant contribution to climate neutrality in Europe. There are two major hydrogen producers in Slovakia. These include chemical plants: Fortischem and Duslo located in Nováky and Šala. The hydrogen they produce is used entirely in their own production processes, so it is not possible to export it. It is worth mentioning that most of the hydrogen used in the Slovak chemical industry is currently produced from fossil fuels [48].

Slovakia is the country with the most dynamic growth of energy production from RES among all V4 countries. The share of renewable sources, which mainly include wind and water, in gross final energy consumption in 2020 was about 17.3%. This means that Slovakia has more than met the EU requirement of 14% set for 2020 [49]. The growth of RES and nuclear in energy consumption is to compensate for the shift away from coal, which accounts for about 11% of Slovakia’s energy mix. According to government plans, coal-fired power plants, as well as lignite mines, are to be closed by 2023 (with one exception). This represents an acceleration of the process of moving away from emission-intensive energy sources. In view of the above, the Slovak government also aims to support hydrogen energy. In June 2021, the National Hydrogen Strategy was approved by the government. The strategy includes a wide range of areas of hydrogen use, including the chemical, petrochemical, metallurgical, and gas industries. Among the most ambitious plans is the production of hydrogen by using surplus energy from Slovakia’s nuclear power plants or from existing natural gas infrastructure. The greatest support in the development of the hydrogen market will go to the automotive industry, as this sector is the driving force of the country’s economy with a 13% share of Slovak GDP or 54% of industrial production. Therefore, the biggest challenge facing the Slovak automotive industry is the decarbonization of the sector and production of hydrogen powered cars and public and long distance transport vehicles [50]. It should be added that the first tangible results of the mentioned strategy are already visible in the automotive sector, with two hydrogen refueling stations being put into operation in Slovakia in 2022 [51].

The Slovak hydrogen strategy indicates the areas around which the hydrogen market will be developed but does not set specific implementation goals in a time perspective. The hydrogen strategy focuses its attention on the following areas of the economy:

- Chemical and petrochemical industry (hydrogen will serve as an energy carrier in various chemical reactions in energy-intensive production segments and as a chemical substance so far. The most important task facing this sector is the search for perspective solutions to replace the production of hydrogen using fossil fuels or to modify it by introducing technologies to capture or reuse the greenhouse gases produced).

- The steel and metallurgical industries (the steel and metallurgical industries together with the automotive industry represent the backbone of the Slovak economy and at the same time the largest emitters of CO2. Therefore, as in the chemical and petrochemical industries, it will be necessary to replace the existing brown hydrogen with green hydrogen).

- The gas industry (the Slovak government aims to introduce hydrogen into the existing natural gas network in order to displace the use of methane and reduce emissions. This action requires the introduction of innovative logistical solutions for the transportation, distribution and storage of gas. Underground natural gas storage facilities will be used for hydrogen storage).

- Heating (the use of hydrogen in this sector can have a positive impact on reducing primary energy consumption. Moreover, using the seasonal accumulation of hydrogen during the summer and using it in times of energy shortage in the system will allow balancing the demand).

- Transport (the introduction of fuel cells in the transport sector will allow the development of a market for new propulsion systems. Slovakia as an important car manufacturer in Europe, creating a real alternative to combustion engines and electromobility, intends to build a network of hydrogen fueling stations) [52].

4.4. Hungary

Hungary, being a country almost entirely dependent on imports of key fossil hydrocarbons, believes that hydrogen will play an important role in its path towards climate neutrality. In Hungary, as in other V4 countries, hydrogen is produced from natural gas, at a rate of 160,000 tons per year. The produced hydrogen is used in the production of ammonia (2/3 of the production), and the rest is used in oil refining and in the chemical industry.

Hungary was the country with the fastest national hydrogen strategy out of the entire Visegrad group (May 2021). The current document sets goals for the development of the hydrogen market in the country until 2030. The biggest focus is on replacing currently produced high-carbon hydrogen with low-carbon hydrogen, which would significantly reduce greenhouse gas emissions in the industry as well as in the national economy. Renewable hydrogen is recognized in the strategy as an alternative fuel that provides a clean solution for mobility. Thus, hydrogen can serve Hungary, which is highly dependent on fossil fuels, as a link between the electricity and natural gas sectors, while greening the gas sector and thus increasing the country’s gas security [53]. Hungary’s hydrogen sector development efforts are focused on the following points:

- -

- Production of large amounts of low- and zero-carbon hydrogen (the technical potential of renewable electricity generation in Hungary is three times higher than the projected electricity demand in 2030, so there is an opportunity to use the potential excess capacity of RES electricity generation to produce hydrogen through electrolysis). Power-To-Gas (P2G) facilities producing zero-emission hydrogen can play a key role in balancing the electricity system and addressing regional and local grid issues.

- -

- Partial decarbonization of hydrogen consumed by industry: gradual replacement of gray hydrogen, with low-carbon hydrogen-turquoise, and eventually green. By 2030, the first pilot plants producing green (or low-carbon) hydrogen will be operational. Moreover, Hungarians also plan to create two hydrogen valleys in the northeastern part of the country and in the Transdanubian region.

- -

- Green transport: The use of hydrogen in the propulsion of trucks and buses, and from 2025 in passenger vehicles.

- -

5. Development of the Hydrogen Market in the V4 Group-Results and Discussion

The development of the hydrogen market in Europe has accelerated significantly. Most EU member states have already published their hydrogen strategies. The rush is necessary as hydrogen is set to become an important part of the energy mix, and it will make it easier to achieve climate neutrality. All of the countries analyzed have transposed the EU Hydrogen Strategy over the past year, creating strategic documents for the development of the hydrogen economy in their country. After the analysis, the conclusion is that the above activities are characterized by a top-down approach with strong state capital participation. Top-down analysis is oriented towards studying the global environment first, hence decisions are made on the basis of global variables, followed by the microenvironment. Thus, the biggest advantage of this approach is better coordination and securing more resources for hydrogen projects by raising external funds for designated projects. An important element in addition to the strategy is the creation of technology maps that define the potential, goals, and pathways to get there in the medium and long term for each segment of the hydrogen economy [56]. Such technology maps have been best prepared by the Poles and the Hungarians, who have divided into periods, indicating the appropriate actions in each period, in an effort to develop the hydrogen market in their country. Czech and Slovak strategies are far from indicating specific solutions and forecasts for the development of hydrogen economy. Most probably, this is due to the small-scale, independent production of hydrogen, small amount of RES (for Czech Republic), and occurrence of difficulties accompanying the RES market expansion due to unfavorable atmospheric and geological conditions affecting the development of this form of energy acquisition. The Czech and Slovak strategies are very general and therefore there are no precise deadlines and details for their implementation. Table 1 presents the goals and actions for creating a hydrogen economy, which are defined in the hydrogen strategies of each of the four V4 countries.

Hydrogen is expected to be an important energy carrier for the entire V4 group to support their decarbonization efforts. All countries announce that their hydrogen production will be carried out using all available methods to obtain low- and zero-emission hydrogen. The Czech Republic, Slovakia and Hungary intend to use energy produced in their nuclear power plants for this process, and Poland will join the group as soon as it has its own first nuclear reactors, small-scale SMRs and later in 2034 two large-scale power units. Hydrogen is also expected to help in the decarbonization of transport, and this sector will see the fastest noticeable change, as all V4 countries intend to implement hydrogen fuel cell vehicles, first in public transport (buses, trains and ferries). Over time, as the technology becomes more widespread, hydrogen filling stations are expected to be systematically expanded, increasing the number of hydrogen-powered passenger cars. In the early years of the hydrogen market, H2 transportation will be by road and rail. All four states declare to start researching the possibility of mixing hydrogen into natural gas and to convert part of their gas networks to hydrogen in the long run. The development of hydrogen infrastructure in the region will be fostered by the participation of all four countries in the European Hydrogen Backbone initiative, in which European gas companies work together to plan a pan-European hydrogen network. This network is expected to be 11,600 km in 2030 and 39,700 km a decade later, connecting the various European hydrogen valleys [58].

The use of conventionally produced hydrogen can reduce carbon dioxide emissions by almost 20%. Renewable hydrogen, on the other hand, is an effective solution for reducing CO2 emissions, hence each country analyzed plans to reduce pollution through its use. Poland is projected to have the largest CO2 reduction (0.7–1.8 Mt CO2 in 2030), but when comparing the total reduction of GHG emissions to the national target for 2030, the best performers are Slovakia and Hungary (1.1–3.3% and 1.4–3.2% respectively).

Undoubtedly, the Polish hydrogen strategy stands out from the strategies published by the other three Visegrad Group countries. First, because Poland is already in third place in Europe as a hydrogen producer, hence it will start from a different place in creating the hydrogen market than the other countries analyzed. Secondly, Polish plans to develop the hydrogen sector are more concrete and far reaching than in the other V4 countries. Polish plans include the creation of five hydrogen valleys. Similar aspirations are held by Hungarians who intend to create two hydrogen valleys, and the Czechs with 1 valley. Moreover, the plan to build 2 GW of electrolyzer capacity in Poland by 2030 is also very ambitious, especially when compared to the 240 MW of electrolyzer capacity in Hungary at the same time, or the announcement of 5 GW of electrolyzer capacity in Germany, with a more advanced hydrogen economy. Part of the hydrogen strategy of the Czech Republic and especially Slovakia for many of these proposals lacks deadlines and details regarding implementation.

Green hydrogen production has been tested for some time, but its development on a larger scale will occur when it receives public support and production costs are reduced. It is worth mentioning that only when the share of RES energy production in the region increases, will zero-emission hydrogen production flourish.

Certainly, the first step that will allow the development of the hydrogen market in the discussed countries will be the implementation of appropriate legal regulations on the safety of H2 use. The removal of barriers to the development of the hydrogen economy may take place after the adoption of a comprehensive hydrogen legislative package, especially the Hydrogen Law. The legal solutions it contains will define the rules for hydrogen production and storage, as well as technical supervision of H2 handling, transportation and storage facilities. In parallel, fiscal incentives should be implemented [59]. The European Hydrogen Strategy directly points to the need for public support from EU funds and European Investment Bank financing, but it should not be excessive. Therefore, in the current decade, V4 countries will base the development of their hydrogen technologies on EU subsidies. It is worth mentioning that, in connection with the EU CO2 reduction goals, the Community intends to financially support clean hydrogen production technologies first. The production of low-emission hydrogen will be supported in the short and medium term in order to spread this form of energy acquisition in various industries as soon as possible [60,61].

In 2022, the European Commission approved the award of public subsidies to support research into the development of hydrogen technology in the amount of EUR 5.4 billion [62].

So far (2019), the largest funds among all member states in this area have been allocated by the governments of Germany (EUR 45 million), France (EUR 38 million), and Italy (EUR 10 million), and this will also be the case in the next decade. Unfortunately, Poland and other V4 countries are still at the end of the ranking, as their expenses are approx. 40% lower than in the leading EU countries [63]. It is worth adding that Poland allocated the most funds for R&D in this field among the countries of the Visegrad Group (in 2002–2017 it was EUR 24 million, and Hungary EUR 1.2 million) [64].

In each country, the pace of development will depend on various factors: the structure of the industry and the volume of production of grey and turquoise hydrogen, as well as the rate of development of RES. The development of the hydrogen market will significantly strengthen the economy by creating new jobs and increasing GDP, enable the integration of green energy into the electricity system, and reduce the carbon footprint.

6. Conclusions

In today’s energy uncertain times, hydrogen is emerging as an energy carrier that can help countries in the future to solve the problem of galloping energy and fuel prices and their scarcity, but also widespread energy poverty. In a word, the energy crisis in which Europe found itself after Russia’s attack on Ukraine and the need to give up Russian raw materials accelerated the development of the hydrogen economy in the world. The countries of the Visegrad Group are looking for solutions enabling the transition to clean energy, hence vigorous measures are taken to introduce hydrogen into the energy sector.

The expansion of hydrogen will certainly change the relationship between exporters of fossil fuels and importers, as there will be competition from new hydrogen producers. Hence, changes in trade flows will generate new economic and political alliances. Hydrogen will play an important role in the energy transition of all Visegrad countries, but to a different extent. Its largest share in decarbonizing the industrial sector is expected to take place in Poland. This country is most likely to become a key player in the hydrogen market in the region, as the relatively even distribution of gas and oil resources across the country eliminates the need to develop new energy transmission infrastructure. In addition, a fairly well-developed network of gas and electricity infrastructure, numerous refineries, liquefied natural gas import terminals, and underground gas storage facilities will enable hydrogen production.

Hydrogen will help other countries of the group to decarbonize the largest sectors of their economy, which are also the largest emitters of CO2, such as the steel and metallurgical industry in Slovakia or the chemical and cement industry in the Czech Republic. However, the share of hydrogen in their decarbonization is expected to be medium in scope in the Czech Republic and Hungary. This is due to the low scale of independent hydrogen production, meaning that these countries will have to import. It will be very important to use hydrogen in heating, which will have a positive impact on reducing primary energy consumption. The introduction of fuel cells to the transport sector along with electromobility will allow for the complete elimination of CO2. At the same time, the market for new propulsion systems will develop in this part of Europe.

The V4 countries, compared to other EU countries, have a relatively small technological potential in the field of a hydrogen economy, which is reflected in the small number of specialized companies and expenditure on R&D. For this reason, the biggest problem for the development of innovations in the area of hydrogen is the low maturity of the market and insufficiently targeted research; hence the need to be open to greater national and international cooperation.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Capros, P.; Zazias Evangelopoulou, G.S.; Kannavou, M.; Fotioua, T.; Siskos, P.; De Vita, A.; Sakellaris, K. Energy-system modelling of the EU strategy towards climate-neutrality. Energy Policy 2019, 134, 110960. [Google Scholar] [CrossRef]

- Kochanek, E. The Energy Transition in the Visegrad Group Countries. Energies 2021, 14, 2212. [Google Scholar] [CrossRef]

- Dyduch, J.; Skorek, A. Go South! Southern dimension of the V4 state’s Energy policy strategies–An assesment of viability and prospects. Energy Policy 2020, 140, 111372. [Google Scholar] [CrossRef]

- Lebrouhia, B.E.; Djoupo, J.J.; Lamrani, B.; Benabdelaziz, K.; Kousksou, T. Global hydrogen development-A technological and geopolitical overview. Int. J. HyDrogen Energy 2022, 47, 7017. [Google Scholar] [CrossRef]

- Kovač, A.; Paranos, M.; Marciuš, D. Hydrogen in energy transition: A review. Int. J. Hydrogen Energy 2021, 46, 10023. [Google Scholar] [CrossRef]

- Mirowski, T.; Janusz, P. Hydrogen in Energy balance–selected issues. Zesz. Nau-Kowe Inst. Gospod. Surowcami Miner. I Energią Pol. Akad. Nauk 2018, 102, 53. [Google Scholar]

- Dunn, S.; Cutler, J. Hydrogen. In History of Encyclopedia of Energy Red; Cutler J. Cleveland: Boston, MA, USA, 2004; p. 241. [Google Scholar]

- Petinrin, M.; Adebayo, M.; Adelowokan, A. A Review on Hydrogen as a Fuel for Automo-tive Application. Int. J. Energy Eng. 2014, 4, 76. [Google Scholar]

- Hart, D. Hydrogen, end uses and economics. In Encyclopedia of Energy Red; Cutler J. Cleveland: Boston, MA, USA, 2004; p. 231. [Google Scholar]

- Henderson, I. A New Era for Airships: Enhancing New Zealand’s Air Power with Lighter-than-Air Technology. J. R. New Zealand Air Force 2019, 5, 90. [Google Scholar]

- Okolie, J.A.; Patra, B.; Mukherjee, A.; Nanda, S.; Dalai, A.K.; Kozinski, J.A. Futuristic ap-plications of hydrogen in energy, biorefining, aerospace, pharmaceuticals and metallurgy. Int. J. Hydrog. 2021, 46, 8888. [Google Scholar] [CrossRef]

- Wiącek, D. Wodór jako paliwo przyszłości. Autobusy 2011, 11, 447. [Google Scholar]

- Basic Information on Hydrogen. Available online: https://www.ien.com.pl/tl_files/pliki/CPE/FAQ_final_EN.pdf (accessed on 5 May 2022).

- Available online: https://pie.net.pl/wartosc-rynku-wodoru-osiagnie-w-2022-r-600-mld-zl-35-proc-wiecej-niz-w-2015-r/ (accessed on 1 September 2022).

- Andersson, J.; Grönkvist, S. Large-scale storage of hydrogen. Int. J. Hydrogen Energy 2019, 44, 11902. [Google Scholar] [CrossRef]

- Mboyi, C.D.; Poinsot, D.; Roger, J.; Fajerwerg, K.; Kahn, M.L.; Hierso, J.C. The Hydrogen-Storage Challenge: Nanoparticles for Metal-Catalyzed Ammonia Borane Dehydrogenation. Small 2021, 17, 2102759. [Google Scholar] [CrossRef]

- Sakintuna, B.; Lamari-Darkrim, F.; Hirscher, M. Metal hydride materials for solid hydrogen storage: A review. Int. J. Hydrogen Energy 2007, 32, 1121. [Google Scholar] [CrossRef]

- Bünger, U.; Michalski, J.; Crotogino, F.; Kruck, O. Large-scale underground storage of hydrogen for the grid integration of renewable energy and other applications. In Compendium of Hydrogen Energy; Hydrogen Use, Safety and the Hydrogen Economy; Woodhead Publishing: Cambridge, UK, 2016; Volume 4, pp. 133–139. [Google Scholar]

- Egeland-Eriksena, T.; Hajizadeh, A.; Sartori, S. Hydrogen-based systems for integration of renewable energy in power systems: Achievements and perspectives. Int. J. Hydrogen Energy 2021, 46, 31965. [Google Scholar] [CrossRef]

- Global Trends and Outlook for Hydrogen; IEA Hydrogen: Paris, France, 2017; pp. 6–7.

- Polish Hydrogen Strategy to 2030 with an Outlook to 2040; Ministry of Climate and Environment: Warsaw, Poland, 2021; pp. 12–23.

- Safe Use of Hydrogen as a Fuel in Commercial Industrial Applications, Information Publication of the Polish Register of Shipping. 2021. Available online: https://www.prs.pl/uploads/p11i_pl.pdf (accessed on 25 April 2022).

- Different Colors of Hydrogen, Institute of Energy and Fuel Processing Technology. Available online: http://www.ichpw.pl/blog/2021/08/24/rozne-kolory-wodoru/ (accessed on 3 September 2022).

- Ji, M.; Wang, J. Review and comparison of various hydrogen production methods based on costs and life cycle impact assessment indicators. Int. J. Hydrogen Energy 2021, 46, 38614. [Google Scholar] [CrossRef]

- Kakoulaki, G.; Kougias, I.; Taylor, N.; Dolci, F.; Moya, J.; Jäger-Waldau, A. Green hydrogen in Europe–A regional assessment: Substituting existing production with electrolysis powered by renewables. Energy Convers. Manag. 2021, 228, 113649. [Google Scholar] [CrossRef]

- IEA. Global Hydrogen Review. IEA: Brussels, Belgium, 2021; p. 20. [Google Scholar]

- IRENA. Hydrogen from renewable power technology outlook for the energy transition. IRENA: Abu Dhabi, United Arab Emirates, 2018; pp. 13–14. [Google Scholar]

- Grand View Research, Inc. Hydrogen Generation Market Size, Share & Trends Analysis Report By Systems (Merchant, Captive), By Technology (Steam Methane Reforming, Coal Gasification), By Application, By Source, By Region, And Segment Forecasts, 2022–2030, Grand View Reasearch. Grand View Research, Inc.: San Francisco, CA, USA, 2022; p. 7. [Google Scholar]

- World Energy Council. Working Paper National Hydrogen Strategies; World Energy Council: London, UK, 2021; p. 16. [Google Scholar]

- Capurso, T.; Stefanizzi, M.; Torresi, M.; Camporeale, S.M. Perspective of the role of hy-drogen in the 21st century energy transition. Energy Convers. Manag. 2022, 251, 114898. [Google Scholar] [CrossRef]

- Dos Santos, K.G.; Thaís Eckert, K.; De Rossi, E.; Bariccatti, R.A.; Frigo, E.P.; Lindino, C.A.; Alves, H.J. Hydrogen production in the electrolysis of water in Brazil, a review. Renewable Sustain. Energy Rev. 2017, 68, 564. [Google Scholar] [CrossRef]

- Kırtay, E. Recent advances in production of hydrogen from biomass. Energy Convers. Manag. 2011, 52, 1779. [Google Scholar] [CrossRef]

- Kumar, G.; Shobana, S.; Nagarajan, D.; Lee, D.; Lee, K.; Lin, C.; Chen, C.; Chang, J. Biomass based hydrogen production by dark fermentation—recent trends and opportunities for greener processes. Curr. Opin. Biotechnol. 2018, 500, 137. [Google Scholar] [CrossRef]

- Yue, M.; Lambert, H.; Pahon, E.; Roche, R.; Jemei, S.; Hissel, D. Hydrogen Energy systems: A critical review of technologies, applications, trends and challenges. Renew. Sustain. Energy Rev. 2021, 146, 17. [Google Scholar] [CrossRef]

- European Commission. Communication From The Commission To The European Parliament, The Council, The European Economic And Social Committee And The Committee Of The Regions A Hydrogen Strategy for Climate-Neutral Europe; European Commission: Brussels, Belgium, 2020; pp. 1–3. [Google Scholar]

- Sadik-Zada, E.R. Political Economy of Green Hydrogen Rollout: A Global Perspective. Sustainability 2021, 13, 13464. [Google Scholar] [CrossRef]

- Hydrogen Europe. Clean Hydrogen Monitor 2021; Hydrogen Europe: Brussels, Belgium, 2021; pp. 10–13. [Google Scholar]

- Wolf, A.; Zander, N. Green Hydrogen in Europe: Do Strategies Meet Expectations? Intereconomics 2021, 6, 322. Available online: https://www.intereconomics.eu/pdf-download/year/2021/number/6/article/green-hydrogen-in-europe-do-strategies-meet-expectations.html (accessed on 20 March 2022).

- Energy Institute. Analysis of the Potential of Hydrogen Technologies in Poland Until 2030 with Perspective Until 2040; Energy Institute: London, UK, 2020; p. 86. [Google Scholar]

- IDA. Transport 4.0 Development of Electromobility and Hydromobility in the World and in Poland; IDA: Washington, DC, USA, 2021; Volume 1, p. 72. [Google Scholar]

- Gawlik, L.; Mokrzycki, E. Analysis of the Polish Hydrogen Strategy in the Context of the EU’s Strategic Documents on Hydrogen. Energies 2021, 14, 6382. [Google Scholar] [CrossRef]

- Iordache, I.; Bouzek, K.; Paidar, M.; Stehlík, K.; Töpler, J.; Stygar, M.; Dąbrowa, J.; Brylewski, T.; Stefanescu, I.; Iordache, M.; et al. The hy-drogen context and vulnerabilities in the central and Eastern European countries. Int. J. Hydrogen Energy 2019, 44, 19038. [Google Scholar] [CrossRef]

- Janíček, L.; Reichmann, L.L. Hydrogen law and Regulation in The Czech Re-public, CMS Exper Guide. Available online: https://cms.law/en/int/expert-guides/cms-expert-guide-to-hydrogen/czech-republic (accessed on 10 April 2022).

- Available online: https://www.krustecky.cz/vismo/dokumenty2.asp?id_org=450018&id=1764116&n=ucast%2Dv%2Dmezinarodnich%2Dorganizacich%2Dhydrogen%2Deurope (accessed on 7 July 2022).

- IndexBox. Czech Republic-Hydrogen-Market Analysis, Forecast, Size, Trends and Insights; IndexBox: Palo Alto, CA, United States, 2021. [Google Scholar]

- Gołębiowska, M.; Paszkowski, M. The Coming Hydrogen Revolution in Central Europe-Benefits and Challenges: IEE Comment. 2020. Available online: https://ies.lublin.pl/komentarze/nadchodzaca-wodorowa-rewolucja-w-europie-srodkowej-korzysci-i-wyzwania/ (accessed on 25 April 2022).

- Ministry of Industry and Trade of the Czech Republic. Hydrogen Strategy of the Czech Republic; Ministry of Industry and Trade of the Czech Republic: Prague, Czech Republic, 2021; pp. 53–55.

- Werner, O.; Hydrogen Law and Regulation in Slovakia. CSM Expert Guide 2021. Available online: https://cms.law/en/int/expert-guides/cms-expert-guide-to-hydrogen/slovakia (accessed on 30 March 2022).

- Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=File:Share_of_energy_from_renewable_sources_2020_infograph.jpg#filehistory (accessed on 11 June 2022).

- Theisen, N.; Hubatka, S. Slovakia: An Automotive Industry Perspective; GLOBSEC: Bratislava, Slovakia, 2021; p. 5. [Google Scholar]

- Čerpacie Stanice na Vodík v Roku 2021 Nepribudli, Predalo sa Jedno Vodíkové Auto. Available online: https://www.mojelektromobil.sk/slovensko-cerpacie-stanice-na-vodik-prehlad-2021-plany/ (accessed on 10 June 2022).

- Ministry of Economy of the Slovak Republic. National Hydrogen Strategy: Ready for the Future; Ministry of Economy of the Slovak Republic: Bratislava, Slovakia, 2021; pp. 14–18.

- Hungary paves the way for the construction of a hydrogen economy. Available online: https://hungarianinsider.com/hungary-paves-the-way-for-the-construction-of-a-hydrogen-economy-8004/ (accessed on 16 May 2022).

- FCH. Hungary’s National Hydrogen Strategy, Budapest; Fuel Cells and Hydrogen Joint Undertaking: Brussels, Belgium, 2021; pp. 3–4. [Google Scholar]

- FCH. Opportunities for Hydrogen Energy Technologies Considering the National Energy & Climate Plans, Hungary; Fuel Cells and Hydrogen Joint Undertaking: Brussels, Belgium, 2021; pp. 10–13. [Google Scholar]

- Koen, P.A. Technology Maps: Choosing the Right Path. Eng. Manag. J. 1997, 4, 7–11. [Google Scholar] [CrossRef]

- FCH. Brochure: Opportunities for Hydrogen Energy Technologies Considering the National Energy& Climate Plan for: Poland, Czech, Slovakia, Hungary; Fuel Cells and Hydrogen Joint Undertaking: Brussels, Belgium, 2020. [Google Scholar]

- European Union Hydrogen Backbone Report 2020. Available online: https://gasforclimate2050.eu/ehb/ (accessed on 12 June 2022).

- Antas, Ł.; Bocian, M.; Bajek, M.; Giers, M.; Bijoś, K. Hydrogen in Central and Eastern Europe: Perspectives for Development of Hydrogen Economy in Visegrad Group and Ukraine; Esperis: Warsaw, Poland, 2021; p. 10. [Google Scholar]

- EU Funding Programmes and Funds 2021–2027. Available online: https://ec.europa.eu/growth/industry/strategy/hydrogen/funding-guide/eu-programmes-funds_en?msclkid=dcdfd706b5bb11ec8a9623b35e440b8e (accessed on 5 May 2022).

- Andruszkiewicz, M. Hydrogen as an element of economy decarbonization in the light of hydrogen strategy of European Union and Poland. Nowa Energ. 2021, 3, 55. [Google Scholar]

- Available online: https://ec.europa.eu/info/news/state-aid-commission-approves-eu54-billion-public-support-fifteen-member-states-important-project-common-european-interest-hydrogen-technology-value-chain-2022-jul-18_en (accessed on 5 September 2022).

- Gospodarka wodorowa w Polsce. PIE. Policy Pap. 2020, 5, 18.

- Directions for the development of the hydrogen economy in Poland. PIE 2019, 7, 26.

Figure 1.

Hydrogen classification and its use. Source: [29].

Figure 1.

Hydrogen classification and its use. Source: [29].

{kind=link}

Table 1.

Actions taken to develop the hydrogen economy in the Visegrad countries.

| Developing the Hydrogen Economy—Actions | ||||||

|---|---|---|---|---|---|---|

| V4 Countries | Sources of Hydrogen Production | Legislation | Financial Mechanisms | Objectives of Hydrogen Strategy | Environmental Impact | Costs of Investment in Green H2 by 2030. |

| Poland | All low and zero carbon hydrogen production methods:

| lack of fully adapted regulations | Approx. 600 million PLN for hydrogen projects under the "New Energy" Program of the National Fund for Environmental Protection and Water Management from 2021 r. About 320 million under the "Green Public Transport" program from 2021 |

| Reduction of GHG emissions by 0.7–1.8 Mt CO2 in 2030, corresponding to 0.7–1.8% of the total GHG emission reduction from the 2030 target. | EUR 7.5 billion by 2030. |

| The Czech Republic | Low carbon methods of hydrogen production:

| Act on Fuels and Stations (Zákon č. 311/2006 Sb.)

| Modernizační fond- measures for development of alternative fuels (LNG, CNG, H2, electromobility) in transport (vehicles, stations); Operational Programme-Transport (OPD)- 102 million CZK for hydrogen stations |

| Reduction of greenhouse gas emissions by 0.2–0.6 Mt CO2 by 2030, equivalent to 0.7–2.3% of the total greenhouse gas reduction from the 2030 target | approx. EUR 2.6 billion |

| Slovakia | Apart from a general indication that the produced hydrogen should come from zero- or low-carbon sources, the Slovak strategy does not specify specific sources of its origin. It indicates the possibility of H2 production from electrolyzers and the use of nuclear energy. |

| Support for hydrogen only in the sphere of announcements | Slovakia estimates installed capacity in 2030 at 0.5 GW in wind and 1.2 GW in photovoltaics, generating about 2.3 TWh of variable electricity from renewable sources in 2030.

| GHG emission reduction of 0.1–0.4 Mt CO2 in 2030, equivalent to 1.1–3.3% Total GHG emission reduction to 2030 | target approx. EUR 1.3 billion |

| Hungary | The primary energy sources for hydrogen production will be natural gas and renewable energy, but nuclear energy is to be the pillar of production. | Lack of dedicated legislation. Numerous legislative and regulatory acts regulating hydrogen as a chemical raw material, however, there is necessity of amending practically all of those of these documents with respect to the specificity of hydrogen as an energy source (production, storage transmission). | Green Economy Financing System (Ministry of Innovation and Technology)- in 2020. granted over EUR 33 million for 5 H2 projects, including P2G implemented by Hungarian OSM) |

| GHG emission reduction of 0.3–0.7 Mt CO2 in 2030, equivalent to 1.4–3.2% total GHG emission reduction from the 2030 target. | approx. EUR 3.4 billion |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kochanek, E. The Role of Hydrogen in the Visegrad Group Approach to Energy Transition. Energies 2022, 15, 7235. https://doi.org/10.3390/en15197235

AMA Style

Kochanek E. The Role of Hydrogen in the Visegrad Group Approach to Energy Transition. Energies. 2022; 15(19):7235. https://doi.org/10.3390/en15197235

Chicago/Turabian StyleKochanek, Ewelina. 2022. "The Role of Hydrogen in the Visegrad Group Approach to Energy Transition" Energies 15, no. 19: 7235. https://doi.org/10.3390/en15197235

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.